What a word! Just

give Google the opportunity to identify change and it will reveal 348 million

hits. What a popular word! It is

everywhere from the classroom to the boardroom. It represents a degree of

impermanence with the current state. I have wrestled with ‘change’ as it

applies to the business world for quite some time. As the entire world continues to form and

transform one would have to ‘change’ just to stay the same.

“If you want things to

stay as they are, things will have to change” – Giuseppe Tomasi di

Lampedusa in Il Gattapardo

Organizational transformation is probably the most

publicized use of ‘change’.

Organizations undergo a series of formation and transformation for a

multitude of reasons ranging from increasing market dominance to simple

continuance. In her recent article Implementing Change, Merge

Gupta-Sunderji unpacks the different elements of organizational change of

culture. All of the elements of change

are in reference to how they impact employees.

Primary change is probably the easiest corporate change to

implement and it has no impact on employees.

This type of change doesn’t have any impact on employees’ day-to-day

activities. Secondary change begins to

encroach on employee behavior. However,

it is still in direct alignment with their current activities. Secondary change would take the form of

increasing customer service in a service oriented organization.

Finally tertiary change the ‘change’ with the greatest

depth. With tertiary change the core culture of the organization must under go

a complete transformation from the ‘old methods’ to an adoption of the ‘new

methods’. Tertiary change comes down

from the leader; the vision must be ‘sold’ to every member of the

organization. Each employee must see the

value of the new methods, embrace the vision but more importantly must ‘buy-in’

on a very personal level.

Merge walks the reader through the steps of orchestrating

organization cultural change, from the leader’s presentation of the vision, the

leader’s fielding of questions, empowerment through training and then

ultimately through reward and recognition.

Merge concludes that cultural transformational change is gradual and

leaders must be patient.

It has been my experience that underlying all cultural

transformation there are deep underlying elements that require acknowledgement. Any leader seeking organizational

transformation must have the respect of the organization. This goes beyond ‘lip service’, the team must

believe that the leader is credible, knowledgeable and acting in the best

interest of the organization. Without

this fundamental element of belief in the leader all transformation change is

just a pipe dream.

The second most critical element to begin paving the way for

transformation requires each person being able to see how they benefit from the

change. Without precipitating a

tangential discussion, humans are basically greedy. Therefore any type of change that is to occur

in the organization, employees must understand how the transformation will

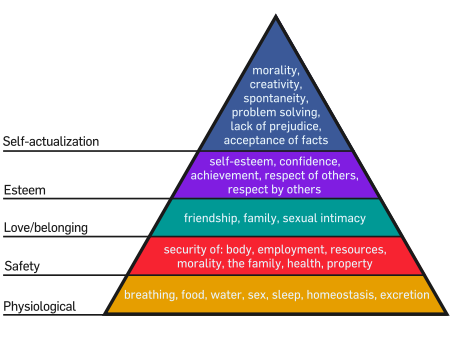

affect them; people need to see how it brings them benefit. Reaching to Abraham

Maslow’s Hierarchy of Needs, people must satisfy lower level needs before

moving up the hierarchy.

As basic needs are satisfied, higher level needs become

exposed and then addressed. By way of an

example, if a corporate transformation fully addresses one’s psychological needs

this change will pave the way for the person to seek fulfillment of their

self-actualization needs. If the employee cannot see how their needs are met or

importantly how the transformational change will meet more of their needs, the

entire process of transformation will be derailed. It is because of this hierarchy of human

needs that any transformation that focuses on attrition will not be received

well or orchestrated well, other than at the executive level.

Good leaders know the power of the carrot and the stick in

achieving goals. Through Maslow’s model,

leaders are able to demonstrate how more of ones’ needs can be met as a

precipitate of adopting the new methods and embracing organizational

change. At the same time the stick is

the combatant for those not embracing the transformation. However, those seeking to preserve their

position in the hierarchy often undertake silent conformity to transformation;

they go through the motions of transformation but not committed to the outcome.

Along with those who are in silent conformity, often in the

midst of corporate transformation there are those who believe they have some

‘special knowledge’ that renders the leader’s vision futile. They don’t embrace the actualization of

themselves to a greater potential.

Instead these individuals, operating on their own self-centered

motivation are the cancer that permeates the organization, to undermine the

transformation. Slowly they infect the

minds of the team to undermine the vision of leaders. Sadly, these sly individuals go through the

motions of compliance, like those silent conformists, but are actively undermining

the transformation.

For true cultural transformation to succeed the leader must

know their troops and build rapport of mutual trust. At the same time the leader must be able to

identify those who are silent conformists as they are only parasites on the

organization. More importantly identify those who are cloaked as silent

conformists but are creating the political undertow in efforts to derail

corporate transformation. There are many forces acting against transformation

and the savvy leader must always be aware of the playing field.